Ever wonder why some forex brokers feel rock-solid while others feel like a gamble? Most traders think offshore licences mean lax oversight, but the data reveals a stark split , a handful of offshore regulators enforce strict fund-segregation rules while the vast majority leave client money unprotected. In the next few minutes we’ll break down exactly how regulation works, which bodies you should be looking at, and what that means for your money , so you can trade with confidence, not confusion.

This forex broker regulation guide covers everything you need to know: why regulation matters, who the key regulators are, how to verify a broker’s license, what compliance obligations mean for you, and how to spot red flags. By the end, you’ll have a clear checklist to evaluate any broker.

Step 1: Understand Why Forex Broker Regulation Matters

Regulation is the safety net that protects your money. Without it, a broker could mix your funds with their own, offer crazy use that blows your account, or even disappear overnight. That’s not just fear-mongering , it’s happened many times.

The core point is simple: regulated brokers must follow strict rules. Those rules include keeping client money in separate bank accounts (segregation), maintaining minimum capital, and submitting to regular audits. For example, the UK’s FCA requires £125,000 (≈ $155k) minimum capital for STP brokers and mandates segregated accounts, plus backs deposits up to £50,000 per trader with the Financial Services Compensation Scheme (FSCS). In the US, the CFTC and NFA demand even more: $1 million for CFTC-registered firms and a whopping $20 million for combined CFTC & NFA entities. They also require written segregation policies under CFTC Reg 1.20.

“The difference between a regulated and unregulated broker can be the difference between sleeping easy and losing everything.”

Then there’s the other end of the spectrum. Many offshore jurisdictions , like Vanuatu (VFSC), Seychelles (FSA), and Mauritius (FSC) , start at a minimum capital of just $50,000. That’s a fraction of what’s needed in developed markets. They also allow “unrestricted” use, which means you could trade with 500:1 or more. And here’s the scary part: out of 29 broker-jurisdiction entries analyzed, only 10% mentioned any fund segregation requirement. That means in most offshore setups, your money isn’t protected if the broker goes bust.

Why should you care? Because regulation directly affects your risk. A regulated broker keeps your money safe, limits your downside with sensible use caps, and gives you recourse if something goes wrong. The trade-off is that you may have less use. But that’s a good thing , higher use amplifies losses just as quickly as gains. As one Content from https://www.forexbrokers.com/guides/high-use-brokers notes, “high use has the potential to amplify losses as well as gains.”

Think about it this way: regulation is like a seatbelt. It’s not just red tape , it’s protection. And the first step in using this forex broker regulation guide is accepting that you want that protection.

Bottom line:Understanding why regulation matters is the foundation of safe trading , it directly protects your capital and reduces the chance of fraud.

Step 2: Identify Key Regulatory Bodies Worldwide

Not all regulators are created equal. Some are strict, well-funded, and consumer-focused. Others are more lax , sometimes deliberately, to attract brokers that can’t meet tougher standards. This forex broker regulation guide helps you sort them out.

Here are the major players you need to know:

| Regulator | Jurisdiction | Min Capital | Max Use (Retail) | Fund Segregation | Compensation Scheme |

|---|---|---|---|---|---|

| FCA (UK) | United Kingdom | £125,000 (~$155k) | 1:30 (ESMA limits) | Yes | FSCS up to £50,000 |

| CFTC/NFA (US) | United States | $20 million (combined) | 1:50 (major pairs) | Yes | No (but strict audits) |

| CySEC (Cyprus) | Cyprus (EU) | €730,000 (~$800k) | 1:30 (ESMA) | Yes | ICF up to €20,000 |

| ASIC (Australia) | Australia | AUD $1 million | 1:30 (ASIC cap) | Yes | No |

| FSC (Mauritius) | Mauritius | $50,000 | Unrestricted | Rarely required | No |

| VFSC (Vanuatu) | Vanuatu | $50,000 | Unrestricted | Not required | No |

As you can see, there’s a huge gap. On one side, you have the US, UK, EU, and Australia , high capital, mandatory segregation, compensation schemes, and tight use caps. On the other, offshore centres like Vanuatu, Seychelles, and Mauritius offer low barriers, no caps, and little protection.

Why do brokers choose offshore then? Cost and flexibility. A broker can set up with $50,000 and offer unlimited use, attracting traders who want to gamble big. But it’s a two-edged sword: when the market moves against you, you could lose more than your deposit, and if the broker fails, your funds may vanish.

Another key point: some countries have unique rules. Poland’s KNF allows 1:100 use only for professional traders. Switzerland’s FINMA doesn’t impose EU-style caps, so brokers like Swissquote can offer up to 100:1. And in the EU, ESMA’s 1:30 cap applies to all retail clients.

So how do you decide? If you want maximum safety, choose a tier-1 regulator (FCA, CFTC, ASIC, CySEC). If you’re an experienced trader comfortable with higher risk, an offshore license might offer more use , but only if you fully understand the protection gap.

Every regulated broker should display its license number and regulator on its website. If you can’t find it easily, that’s a red flag. In the next step, we’ll show you exactly how to verify that license.

Bottom line:Identifying key regulatory bodies helps you understand the protection level each broker offers and avoids risky jurisdictions with no safety nets.

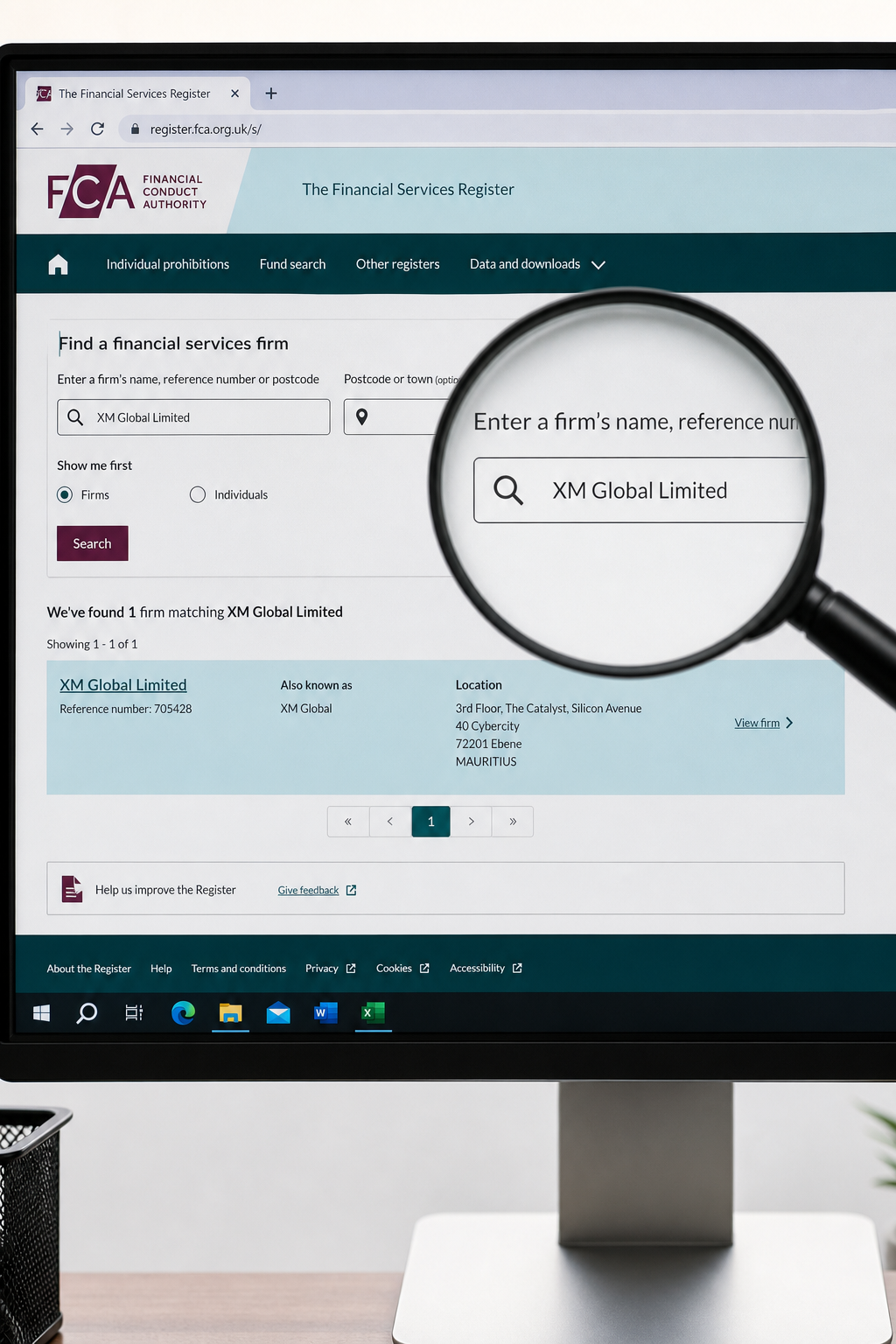

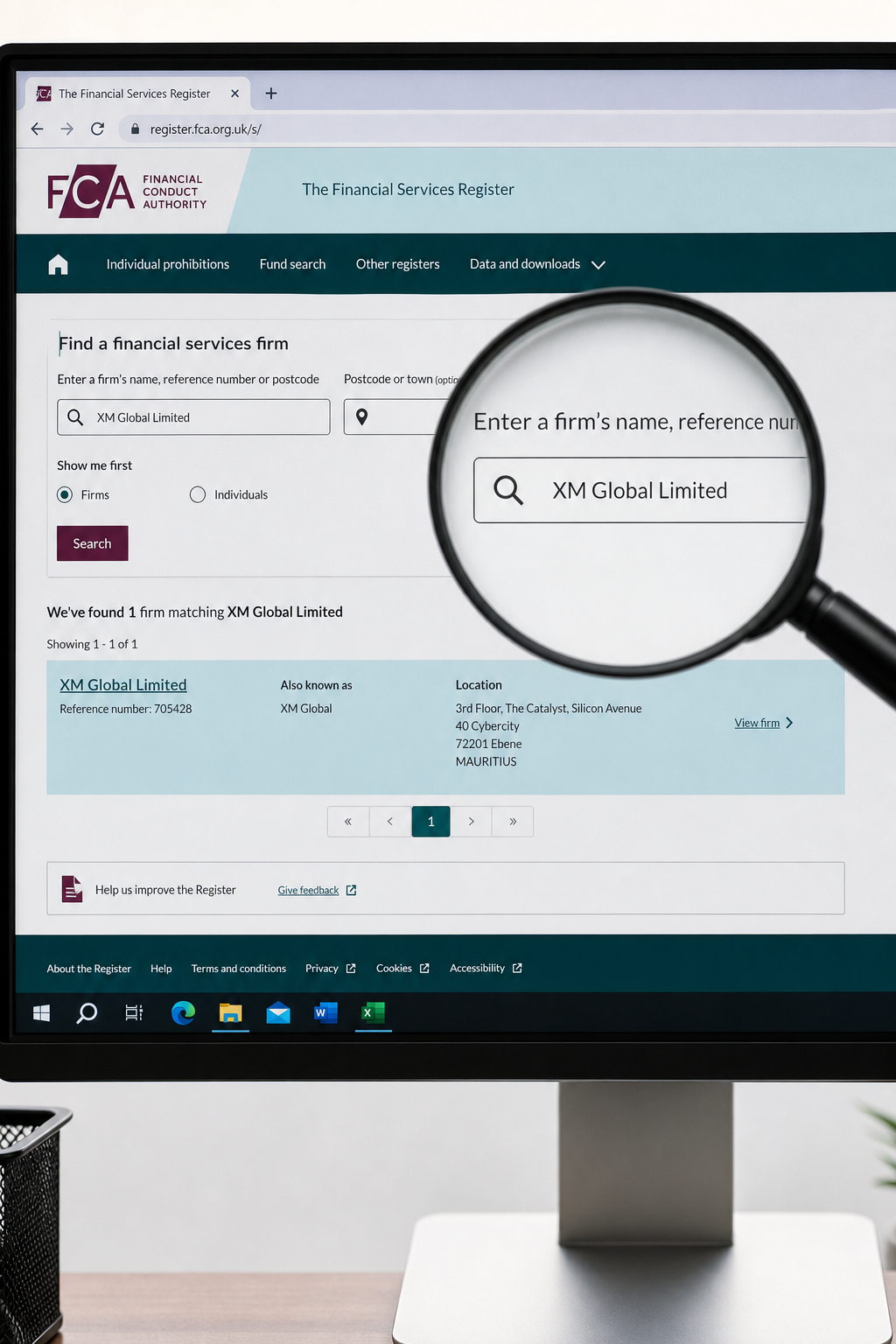

Step 3: How to Verify a Broker’s License Step by Step

You’ve found a broker that looks good. They claim to be regulated by the FCA or ASIC. But how can you be sure? This is the most critical step in the forex broker regulation guide. Let’s walk through it methodically.

Step 3.1: Find the License Claim

First, locate the broker’s regulatory information. It’s usually at the bottom of their website (footer) or in a “Regulation” or “About” page. Look for a registration number. Common formats: for FCA it’s a 6-digit number (e.g., 123456); for CySEC it’s a 5-digit number; for ASIC it’s an AFSL number. Write it down.

Step 3.2: Go to the Official Regulator’s Website

Do NOT click a link from the broker’s site. Open a new browser tab and type the regulator’s official URL yourself. Trusted regulators have websites with .gov or .org domains. For instance:

- FCA: FCA Financial Services Register

- CFTC/NFA: NFA BASIC

- ASIC: ASIC Connect

- CySEC: CySEC Regulated Entities

Step 3.3: Search for the License Number

Use the search tool on the regulator’s site. Enter the license number exactly as shown. The result should show the firm’s name, the license number, status (e.g., “Authorised”), and activities they are permitted to conduct. Make sure the name matches the broker exactly. If the status is “No longer authorised” or “Withdrawn”, that’s a huge red flag.

Step 3.4: Check the Details

Now look deeper. Does the regulator allow the broker to hold client money? Is there any restriction on certain activities? For example, the FCA register shows whether a firm can hold client money. If it cannot, that means your funds are not segregated , a major risk. Also, check if the firm is authorised for forex trading specifically (some licenses only cover CFDs or spread betting).

Step 3.5: Cross-Reference with the Broker’s Website

Ensure the registered address and phone number match what’s on the broker’s website. Scammers sometimes fake registration by using a real license number but changing the address. If the regulator’s details differ, contact the regulator to verify.

Step 3.6: Use Additional Verification Tools

Some independent websites provide lists of regulated brokers. While not official, they can help you spot discrepancies. For example, the ForexBrokers.com high-use guide includes the regulatory status for each broker. But always confirm with the official register.

Remember, even if a broker is regulated, the level of protection varies. A CySEC-regulated broker offers an Investor Compensation Fund up to €20,000 , less than the FSCS’s £50,000. And an offshore license from Vanuatu offers no scheme. So after verifying, you also need to evaluate the quality of regulation.

Let’s say the broker passes all checks. Great. But what about their ongoing obligations? That’s where compliance comes in, and it directly impacts your trading experience.

Step 4: Understand Compliance Obligations and Their Impact on Traders

Regulation isn’t just about having a license. Brokers must follow a set of rules known as compliance obligations. These rules affect everything from how they advertise to how they handle your orders. Understanding them helps you know what to expect and what to demand.

Client Fund Segregation

This is the big one. Regulated brokers must keep client money in separate accounts, away from their own operating funds. If the broker goes bankrupt, your money should still be yours. The US CFTC requires written segregation policies under CFTC Reg 1.20. However, many offshore jurisdictions do not mandate this, meaning brokers can use client money for their own purposes , a recipe for disaster.

Risk Disclosures

Brokers must provide clear risk warnings. In the US, NFA rules require that brokers give retail customers a risk disclosure statement that includes the percentage of accounts that lost money in the previous quarter. That’s transparency. If a broker hides this information or makes trading sound easy, be suspicious.

Use Limits

As we’ve seen, use caps vary. EU brokers can’t offer more than 1:30 to retail clients. US brokers cap at 1:50 for major pairs. Offshore brokers may advertise 1:500 or more. Compliance with use limits is a sign that the broker is following the rules. Higher use increases your risk of a margin call, but it also means the broker is taking less risk themselves.

Reporting and Audits

Regulated brokers must submit regular financial reports and undergo audits. This ensures they have enough capital to cover client positions. If a broker is not audited, you can’t trust their financial health.

Negative Balance Protection

This is a critical consumer protection. In the EU, brokers must ensure you can never lose more than your account balance. In the US, this is also required. But offshore brokers often don’t offer it. Without it, you could end up owing money if the market gaps against you , a debt the broker can chase you for.

How do these obligations affect you as a trader? First, they give you peace of mind. Second, they create a level playing field. Third, they limit the broker’s ability to manipulate prices or delay withdrawals. If a broker takes shortcuts on compliance, it’s likely they’ll take shortcuts with your money too.

One more thing: compliance also affects account opening. Regulated brokers require more paperwork , ID, proof of address, financial information. This can feel intrusive, but it’s part of Know Your Customer (KYC) rules. These rules help prevent money laundering and fraud. If a broker lets you open an account with just an email and no documents, that’s a red flag.

So when you’re comparing brokers, look for ones that adhere to strict compliance. It’s not just bureaucracy , it’s your safety net.

Step 5: Stay Updated on Recent Changes and Red Flags

Regulation isn’t static. New rules are adopted, and old loopholes are closed. Staying informed is part of being a responsible trader. This forex broker regulation guide helps you spot when things change.

2025-2026 Updates

Several important changes are shaping the landscape. In the EU, ESMA’s product intervention measures have been renewed, maintaining the 1:30 cap. But some regulators are tightening further. For example, Poland’s KNF has restricted use to 1:100 only for professional clients. In Australia, ASIC has introduced new rules around CFD trading, including a ban on certain binary options and tighter use limits for retail traders. The US remains strict, with the CFTC and NFA actively enforcing capital requirements.

On the offshore side, some jurisdictions are starting to improve. For instance, the British Virgin Islands (FSC) has introduced more strong anti-money laundering rules. However, many still lack basic protections. The key is to watch for changes , a broker that was once considered safe might lose its license, or a regulator might enhance its requirements.

Red Flags Checklist

Here are warning signs that a broker may not be as regulated as they claim:

- They claim regulation by a well-known body but the license number doesn’t match

- The regulator’s website shows a different name or address

- They are not on the official register at all

- They pressure you to deposit quickly with bonuses or high returns

- They have a history of customer complaints about withdrawals

- They are based in a high-risk jurisdiction (e.g., St. Vincent and the Grenadines, which does not regulate forex brokers)

- They offer extremely high use (e.g., 1:1000) without any warning

- They don’t provide a clear risk disclosure or account opening documents

A recent analysis of 29 broker entries found that only 10% mention fund segregation requirements in offshore regulations. That means 9 out of 10 offshore brokers may not segregate client funds. If you trade with one, your money could be at risk if the broker becomes insolvent. Always check the specific license conditions.

How to Stay Updated

Bookmark the official regulator sites and check occasionally. Follow reputable financial news sources. Some sites like GlobeGain discuss regulation trends. Also, join trader forums but verify anything you hear there. And use our internal guide How to Choose a Forex Broker: A Step‑by‑Step Guide for more tips on evaluating brokers.

Finally, remember that regulation is only one piece of the puzzle. Even a fully regulated broker can mismanage risk or have poor execution. Always test with a demo account first, start small, and monitor your broker’s performance.

Frequently Asked Questions

What is forex broker regulation?

Forex broker regulation refers to the oversight and rules imposed by government or independent bodies on forex brokers. These rules are designed to protect traders by ensuring brokers maintain capital, segregate client funds, provide clear risk disclosures, and follow fair practices. Regulators like the FCA, CFTC, and ASIC have authority to license, monitor, and penalize brokers that violate rules. In this forex broker regulation guide, we emphasize that choosing a regulated broker is one of the most important decisions you can make as a trader.

Which is the safest forex broker regulator?

The safest regulators are generally those in tier-1 jurisdictions: the UK’s FCA, the US CFTC/NFA, Switzerland’s FINMA, and Australia’s ASIC. These bodies have strict capital requirements (often over $1 million), mandatory fund segregation, and regular audits. The FCA also offers compensation up to £50,000. However, no regulator is foolproof , always verify the broker’s license on the official register. This forex broker regulation guide recommends using the FCA or CFTC as benchmarks for safety.

How can I check if a broker is regulated?

First, find the broker’s license number from their website. Then go to the official regulator’s website and use their search tool. For FCA, use the Financial Services Register; for NFA, use BASIC; for ASIC, use ASIC Connect. Enter the license number and confirm the broker’s name, status, and permissions. If the status is not “Authorised” or the name doesn’t match, do not deposit. This step-by-step verification is crucial in any forex broker regulation guide.

What use can regulated brokers offer?

Use depends on the regulator. In the EU and UK, retail use is capped at 1:30 under ESMA rules. In the US, it’s 1:50 for major forex pairs. Offshore regulators like those in Vanuatu or Seychelles often allow unlimited use. Higher use amplifies both gains and losses. This forex broker regulation guide advises using use conservatively, regardless of the broker’s allowance, because it can quickly lead to account blowups.

What happens if my broker goes bankrupt while regulated?

If the broker is regulated by a body with a compensation scheme, you may recover some of your funds. The UK FSCS covers up to £50,000 per person. CySEC’s ICF covers up to €20,000. However, in the US and Australia, there is no such scheme , though strict fund segregation means your money should be returned after the broker’s administration. Unregulated offshore brokers offer no protection, which is why this forex broker regulation guide stresses picking a strong regulator.

Are offshore forex brokers always bad?

Not always, but they carry higher risk. Some offshore regulators like the BVI FSC or Labuan FSA have improved their standards. However, the majority lack fund segregation and compensation schemes. If you choose an offshore broker, ensure they have a reputable parent company or additional oversight. Always verify their license and check for any warnings from authorities. This forex broker regulation guide recommends that beginners avoid offshore brokers until they fully understand the risks.

What is the difference between a regulated broker and an unregulated one?

A regulated broker must follow strict rules: maintain minimum capital, segregate client funds, provide risk disclosures, and undergo audits. An unregulated broker does none of this. They can mix client money with operational funds, offer excessive use, and refuse withdrawals without legal recourse. In this forex broker regulation guide, we strongly advise trading only with regulated brokers. The extra paperwork and lower use are a small price for safety.

Can I trade forex without a regulated broker?

You could, but it’s extremely risky. Unregulated brokers are not subject to oversight, so you have no guarantee that your funds are safe. Many are scams. Even if they are honest, you have no recourse if something goes wrong. Some traders use unregulated brokers for high use, but you are essentially gambling on the broker’s integrity. This forex broker regulation guide advises against it; there are plenty of regulated brokers that offer fair use and protection.

Conclusion

Regulation is not just a stamp on a broker’s website. It’s the foundation of trust between you and the broker. This forex broker regulation guide has walked you through five steps: understanding why regulation matters, identifying key regulators, verifying licenses, knowing compliance obligations, and staying updated on changes. By following these steps, you can dramatically reduce your risk of falling victim to scams or broker failures.

Remember the key numbers: tier-1 regulators require at least $1 million in capital; offshore ones start at $50,000. Only 10% of offshore entries in our dataset mention segregation, and 97% lack compensation schemes. Those statistics aren’t theoretical , they represent real risk to your money.

So take action. Use the verification steps before you deposit a single dollar. Bookmark the official registers. And never settle for a broker that isn’t transparent about its regulation. Your trading journey should be about learning the markets, not worrying about whether your broker will hold up its end of the bargain.

If you want to dive deeper, check out our How to Choose a Forex Broker: A Step‑by‑Step Guide for more practical advice. And remember, the best time to start trading safely is now.